You may be entitled to the following tax offsets (rebates) and deductions for the year ended 30 June 2021.

Deductions for expenses related to working from home due to the COVID-19 pandemic

If you are working from home due to the COVID-19 pandemic and incur expenses that your employer is not reimbursed, you may be able to claim them as a tax deduction.

The expenses must be directly related to working from home and you need to keep a record of your working from home hours and your expenses. There are three ways you can choose to calculate additional running expenses:

Shortcut method – A deduction of $0.80 for each hour worked from home due to the COVID-19 pandemic is allowed if you incur additional deductible running expenses as a result of working from home.

Fixed-rate method – allows:

- • a rate of $0.52 per hour for the cost of utilities, cleaning and depreciation of office furniture

- • work-related phone and internet expenses, computer consumables and stationery

- • work-related depreciation of a computer, laptop or similar device.

Actual cost method – claim the actual work-related portion of all running expenses, calculated on a reasonable basis. For more details, please refer to the ATO website under ‘employees working from home.

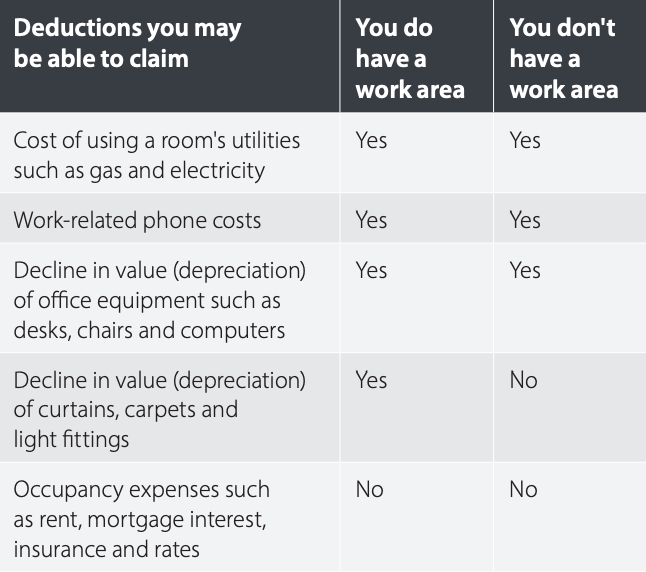

Deductions if your home is not your principal place of business

Private health insurance o ffset

Depending on your income and age, you may be eligible for a tax offset of up to 32.8% on your health insurance. If you haven’t claimed a reduced premium from your health fund, then you can claim an offset in your tax return.

Spouse super contribution o ffset

If you made personal superannuation contributions on behalf of a spouse, there is a tax offset of up to $540 per year.

This is available for spouse contributions of up to $3,000 per year, where your spouse earns less than $37,000 per year, and a partial tax offset for spousal income up to $40,000 per year.

Senior Australians pensioner tax o ffset

If you are eligible for the senior Australians pensioner tax offset (SAPTO), you can earn more income before you have to pay tax and the Medicare levy.

Super tax hints

Super is a tax-effective way to save for retirement. The following section contains some tips to help you maximise your super.

Contribution limits

For the 2020/21 financial year the maximum non-concessional (or after-tax) super contributions are capped at $100,000 per person per year or up to $300,000 over three years using the bring-forward provisions.

The ability to make non-concessional contributions and take advantage of the three-year bring forward provision is subject to your total super balance as at 30 June of the previous financial year, your age and whether you have satisfied the work test (if between ages 67–74).

Concessional contributions, or those made with pre-tax money, are limited to $25,000 per person per year.

Unused concessional contribution caps from the 2018/19 financial year and later years may be used for up to five financial years as long as your total superannuation balance on 30 June before the financial year of contribution is less than $500,000.

Please note, voluntary concessional contributions, such as salary sacrifice or personal deductible contributions, are subject to age restrictions and the work test and work test exemption (if between ages 67–74).

Salary sacrifice

A salary sacrifice strategy allows you to make contributions to super from your pre-tax salary.

Your salary is then reduced by the amount you choose to sacrifice. The benefits of this are two-fold: not only does your super balance increase, but this strategy could also reduce your taxable income and therefore the amount of tax you pay.

Also, super contributions are concessionally taxed at just 15% (up to 30% for individuals with income over $250,000) instead of your marginal tax rate, which could be as high as 47%.

Personal deductible contributions.

Since 1 July 2017, if you are eligible to contribute to super, you may make voluntary personal contributions and claim a tax deduction up to your concessional contribution cap.

This gives you greater flexibility to top up your concessional contributions made by your employer, especially if your employer does not offer salary sacrifice.

For example, you can time your final contributions leading up to 30 June each year and make the most of your concessional contribution limits and the resulting tax benefits.

Super co-contributions

If you receive at least 10% of your income from employment or self-employment and you earn less than $39,837, you may be eligible for the maximum super co-contribution of $500 from the Government for an after-tax contribution to super of $1,000.

The co-contribution phases out once you earn $54,837 or more. The ATO uses information on your income tax return and contribution information from your super fund to determine your eligibility.

Super splitting

If you want to split your super contributions with your spouse, this can usually only be done in the year after the contributions were made.

Therefore, from 1 July 2020, you may be able to split up to 85% of any concessional (or pre-tax) contributions you made during the 2019/2020 financial year with your spouse. Apart from making the most of your super, there are other ways you can minimise your tax liability.

Capital gains and losses

A capital gain arising from the sale of an investment property or shares and capital losses can be used to offset the capital gains.

For example, you may have sold investments that were no longer appropriate for your circumstances and any capital losses realised as a result can be offset against any capital gains you have realised throughout the year.

Unused losses can be carried forward to offset capital gains in future years. Please seek financial advice before making changes to your investments.

Prepaying interest

If you have an investment loan you can arrange to prepay the interest on that loan for up to 12 months and claim a tax deduction in the same year the interest was prepaid.

Negative gearing

Negative gearing is another strategy used to manage tax liabilities.

Geared investments use borrowed funds to enable a higher level of investment than would otherwise be possible. Negative gearing refers to the cost of borrowing exceeding the income generated by the investment.

This excess cost can reduce the tax you pay on other income. If you invest in shares, you may obtain imputation credits which can be used to further reduce the amount of tax you pay.

Income protection insurance

If you hold an income protection policy in your name, then any premium payments you make are tax-deductible.

Resident tax rates for 2020/21

For further information about the 2021 EOFY, please contact us to discuss your financial situation more in depth. ? 02 9898 6777

If you want to know more about Nationwide Financial and our team click here.

The information provided is general in nature. It has been prepared without taking into account any of your individual objectives, financial situation or needs. Before acting on this information, you should consider the appropriateness of the information regarding your own objectives, financial situation, and needs.

Recent Comments