Once you’ve built up a retirement nest egg, it can seem like a lot of money. You might be tempted to take at least some of your superannuation as a lump sum and treat yourself to something.

But remember, with life expectancies on the increase, your money is likely to have to last a long time – maybe even over 20 years. To ensure you enjoy your retirement, you’ll want your money to last at least as long as you do.

Retirement income can come from a variety of sources – a government pension, investment returns such as interest, dividends and rent, and retirement income stream investments especially designed for retirees.

You’ll need to consider how you want to access your superannuation and consider the advantages of leaving it in the superannuation system and drawing a regular income from it.

This post explores three strategies for making the most of your superannuation. Some strategies can provide tax efficiencies or favorable Centrelink treatment.

Some give flexibility in how you can access your money, with no guarantee of how long it will last. Others provide a secure income for a set time.

Three things you could do with your SUPER

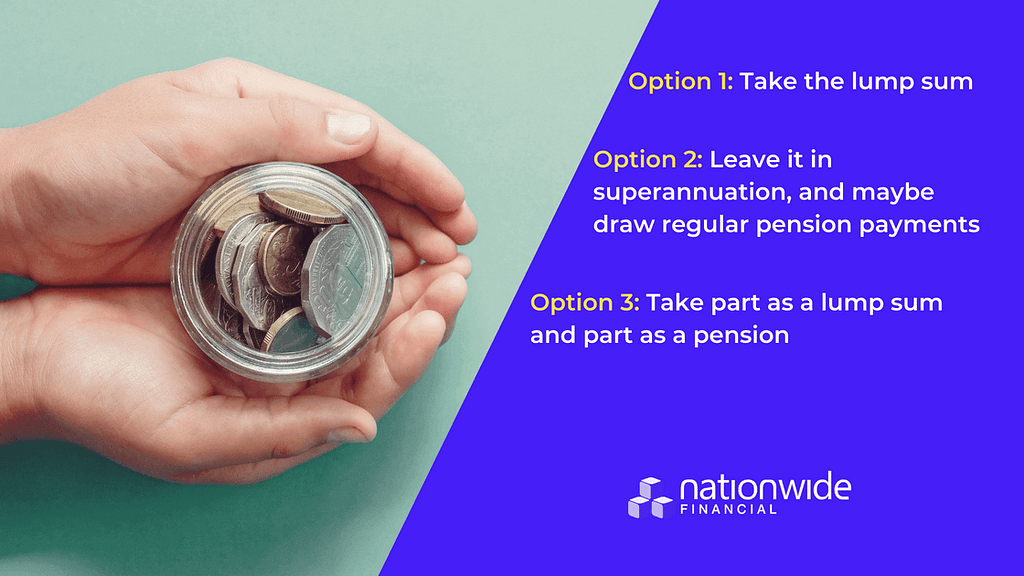

Option 1: Take the lump sum

It might sound good to have such a large amount of money in your hands.

You could go on a holiday, buy a new car or pay off any mortgage you might have left. But before you follow this temptation, remember you’ll need money for many years to come. And by taking money as a lump sum, you might miss out on the tax advantages of leaving it in the superannuation system.

If you do decide to take all your superannuation as a lump sum, it would be wise to re-invest it in a well-planned manner, according to the four principles of wise investing.

Option 2: Leave it in superannuation, and maybe draw regular pension payments

If you decide to keep your money within the superannuation system, the investment earnings on this money will continue to be concessionally taxed at up to 15%.

If you choose to start a pension with your superannuation savings, you will receive a regular income that receives favourable tax treatment.

If you have retired, the earnings and capital gains on the assets supporting the pension are exempt from tax. Generally, there are limits on the amount of superannuation you can use to start a retirement phase pension.

Option 3: Take part as a lump sum and part as a pension

This could offer you the best of both worlds some money for now and some money for later. When planning your retirement income strategy you need to think about whether you have enough investments that give you easy access to funds.

If not, taking a partial lump-sum could provide you with a future cash reserve. Superannuation rules restrict the amount that can be transferred into retirement phase pensions.

Speak to your adviser for further information on how the rules may apply to your circumstances. Be aware though that even if you use all of your superannuation savings to start a pension, you may be allowed to draw extra amounts of money as needed from the pension. Many products allow you to draw extra amounts of money as needed so you could get flexible access to your funds.

A financial adviser can provide a range of value- added services that could help you plan for a successful retirement, including:

• General investment strategies to help you achieve your goals

• Advice on the structure of superannuation and rollovers

• Tax effective strategies

• Centrelink strategies

• Access to streamlined investment services such as master trusts designed to reduce costs

• Planning income streams to help meet individual needs

• Planning future capital growth strategies

• Access to estate planning and risk protection.

OR CALL US TODAY ON 02 9898 6777

If you want to know more about Nationwide Financial and our Team, click here

Disclaimer: The information provided is general in nature. It has been prepared without taking into account any of your individual objectives, financial situation or needs. Before acting on this information you should consider the appropriateness of the information, having regard to your own objectives, financial situation and needs. This publication is prepared by IOOF for: Bridges Financial Services Pty Limited ABN 60 003 474 977 AFSL 240837, Consultum Financial Advisers Pty Ltd ABN 65 006 373 995 AFSL 230323, Elders Financial Planning ABN 48 007 997 186 AFSL 224645, Financial Services Partners Pty Ltd ABN 15 089 512 587 AFSL 237 590, Lonsdale Financial Group Ltd ABN 76 006 637 225 AFSL 246934, Millennium3 Financial Services Pty Ltd ABN 61 094 529 987 AFSL 244252, RI Advice Group Pty Ltd ABN 23 001 774 125 AFSL 238429, Shadforth Financial Group Ltd ABN 27 127 508 472 AFSL 318613 (‘Advice Licensees’). This publication is not available for distribution outside Australia and may not be passed on to any third person without the prior written consent of the Advice Licensees. © How to Retire Successfully is copyright and no part may be reproduced without written permission.

Please note this is general advice, so it may not be suitable for you. For personal tailored advice please see a financial adviser. Past performance does not indicate future performance.

Recent Comments